Large Scale learning with ModelSelector¶

Very often we have many different products, regions, countries, shops…for which we need to delivery forecast. This can be easily done with ModelSelector. ModelSelector though does not bind you to use multiple data partitions and can also serve as convenient layer for accessing relevant information quickly.

[1]:

import pandas as pd

import matplotlib.pyplot as plt

plt.style.use('seaborn')

plt.rcParams['figure.figsize'] = [12, 6]

[2]:

from hcrystalball.model_selection import ModelSelector

from hcrystalball.utils import get_sales_data

from hcrystalball.wrappers import get_sklearn_wrapper

from sklearn.linear_model import LinearRegression

from sklearn.ensemble import RandomForestRegressor

Get Dummy Data¶

[3]:

df = get_sales_data(n_dates=365*2,

n_assortments=1,

n_states=1,

n_stores=2)

[4]:

df.head()

[4]:

| Store | Sales | Open | Promo | SchoolHoliday | StoreType | Assortment | Promo2 | State | HolidayCode | |

|---|---|---|---|---|---|---|---|---|---|---|

| Date | ||||||||||

| 2013-08-01 | 817 | 25013 | True | True | True | a | a | False | BE | DE-BE |

| 2013-08-01 | 513 | 22514 | True | True | True | a | a | False | BE | DE-BE |

| 2013-08-02 | 513 | 19330 | True | True | True | a | a | False | BE | DE-BE |

| 2013-08-02 | 817 | 22870 | True | True | True | a | a | False | BE | DE-BE |

| 2013-08-03 | 513 | 16633 | True | False | False | a | a | False | BE | DE-BE |

[5]:

# let's start simple

df_minimal = df[['Store','Sales']]

Get predefined sklearn models¶

ModelSelector has already predefined large scale of hcrystalball models by their classes. To get this predefined gridsearch use create_gridsearch method. It will allow you to create hundereds of different models in a second. Here for the sake of time, we will use the advantage of the method for cv splits, default scorer etc. and just extend empty grid with two models

[6]:

ms_minimal = ModelSelector(horizon=10, frequency='D')

[7]:

# see full default parameter grid in hands on exercise

ms_minimal.create_gridsearch(

sklearn_models=False,

n_splits=2,

between_split_lag=None,

sklearn_models_optimize_for_horizon=False,

autosarimax_models=False,

prophet_models=False,

tbats_models=False,

exp_smooth_models=False,

average_ensembles=False,

stacking_ensembles=False)

Extend with custom models¶

[8]:

ms_minimal.add_model_to_gridsearch(get_sklearn_wrapper(LinearRegression))

ms_minimal.add_model_to_gridsearch(get_sklearn_wrapper(RandomForestRegressor))

Run model selection¶

Method select_model is doing majority of the magic for you - it creates forecast for each combination of columns specified in partition_columns and for each of the time series it will run grid_search mentioned above. Optionally once can select list of columns over which the model selection will run in parallel using prefect (parallel_over_columns).

Required format for data is Datetime index, unsuprisingly numerical column for target_col_name all other columns except partition_columns will be used as exogenous variables - as additional features for modeling.

[9]:

ms_minimal.select_model(df=df_minimal, partition_columns=['Store'], target_col_name='Sales')

[10]:

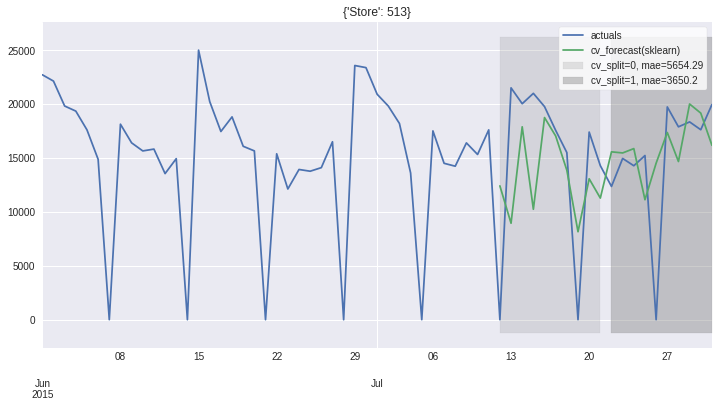

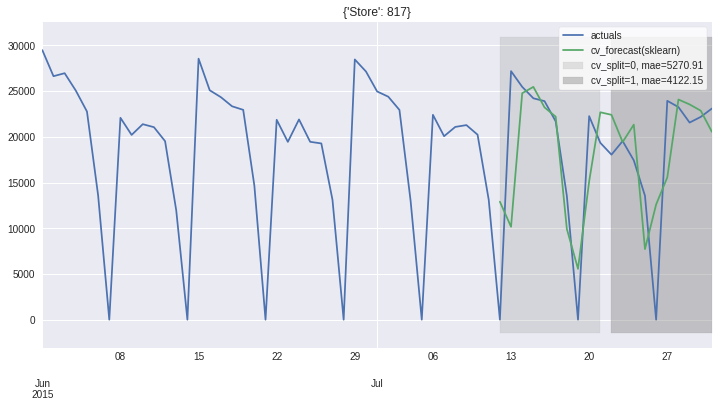

ms_minimal.plot_results(plot_from='2015-06')

Persist and Load¶

ModelSelector stores multiple ModelSelectorResults in given folder as pickle files. As we only have 1 partition, only 1 file is written and loaded back.

[11]:

ms_minimal

[11]:

ModelSelector

-------------

frequency: D

horizon: 10

country_code_column: None

results: List of 2 ModelSelectorResults

paritions: List of 2 partitions

{'Store': 513}

{'Store': 817}

-------------

[12]:

ms_minimal.persist_results('results')

[13]:

from hcrystalball.model_selection import load_model_selector

[14]:

ms_loaded = load_model_selector('results')

[15]:

ms_loaded

[15]:

ModelSelector

-------------

frequency: D

horizon: 10

country_code_column: None

results: List of 2 ModelSelectorResults

paritions: List of 2 partitions

{'Store': 513}

{'Store': 817}

-------------

[16]:

# cleanup

import shutil

try:

shutil.rmtree('results')

except:

pass