Advanced Sarimax Usage¶

If you are not a magician who can easily infer correct SARIMAX orders from looking on PACF (partial autocorrelation function) and ACF (autocorrelation function), you want to rather leverage AutoSarima which finds them for you - set init_with_autoarima to True.

If you want to further configure the search space of AutoARIMA, then you can provide all parameters of pmdarima.arima.AutoARIMA as autoarima_dict arguments.

When you run cross-validation with enabled AutoARIMA (init_with_autoarima), it’s often advisable to find the correct order only during the first fit call and reuse this model on all other splits in order to simulate the out-of-sample performance.

The signature of SarimaxWrapper contains parameters of pmdarima.arima.ARIMA, not AutoARIMA class.

For more parameters check pmdarima docs

[1]:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

plt.style.use('seaborn')

plt.rcParams['figure.figsize'] = [12, 6]

[2]:

from hcrystalball.utils import get_sales_data

df = get_sales_data(n_dates=100,

n_assortments=1,

n_states=1,

n_stores=1)

X, y = df[["Open"]], df['Sales']

[3]:

X

[3]:

| Open | |

|---|---|

| Date | |

| 2015-04-23 | True |

| 2015-04-24 | True |

| 2015-04-25 | True |

| 2015-04-26 | False |

| 2015-04-27 | True |

| ... | ... |

| 2015-07-27 | True |

| 2015-07-28 | True |

| 2015-07-29 | True |

| 2015-07-30 | True |

| 2015-07-31 | True |

100 rows × 1 columns

[4]:

from hcrystalball.wrappers import SarimaxWrapper

[5]:

SarimaxWrapper?

[6]:

model = SarimaxWrapper(

autoarima_dict={'d':1, 'm':7, 'max_p':2, 'max_q':2},

init_with_autoarima=True

)

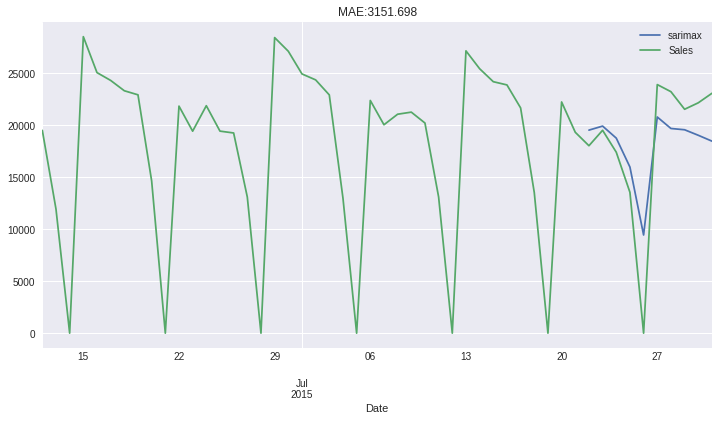

[7]:

preds = (model.fit(X[:-10], y[:-10])

.predict(X[-10:])

.merge(y, left_index=True, right_index=True, how='outer')

.tail(50)

)

preds.plot(title=f"MAE:{(preds['Sales']-preds['sarimax']).abs().mean().round(3)}");

[7]:

<AxesSubplot:title={'center':'MAE:3151.698'}, xlabel='Date'>

And now access the models parameters

[8]:

model

[8]:

SarimaxWrapper(always_search_model=False,

autoarima_dict={'d': 1, 'm': 7, 'max_p': 2, 'max_q': 2},

clip_predictions_lower=None, clip_predictions_upper=None,

conf_int=False, hcb_verbose=True, init_with_autoarima=False,

maxiter=50, method='lbfgs', name='sarimax', order=(0, 1, 2),

out_of_sample_size=0, scoring='mse', scoring_args={},

seasonal_order=(0, 0, 2, 7), start_params=None,

suppress_warnings=True, trend=None, with_intercept=False)

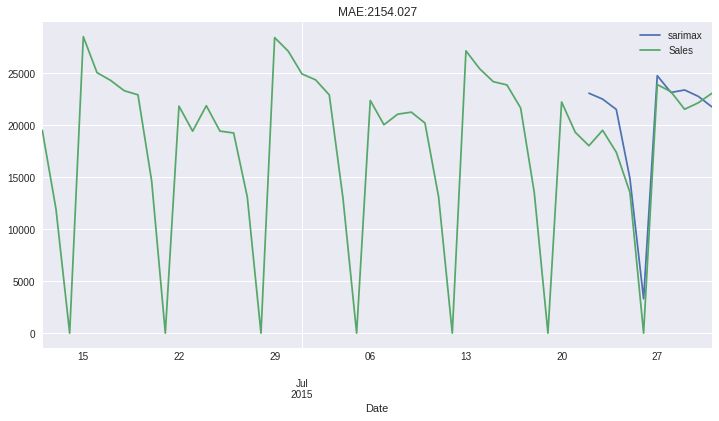

You might also directly pass the orders if you know, what are you doing

[9]:

model = SarimaxWrapper(order=(1, 1, 2), seasonal_order=(1, 0, 2, 7))

[10]:

preds = (model.fit(X[:-10], y[:-10])

.predict(X[-10:])

.merge(y, left_index=True, right_index=True, how='outer')

.tail(50)

)

preds.plot(title=f"MAE:{(preds['Sales']-preds['sarimax']).abs().mean().round(3)}");

[10]:

<AxesSubplot:title={'center':'MAE:2154.027'}, xlabel='Date'>

[11]:

model

[11]:

SarimaxWrapper(always_search_model=False, autoarima_dict=None,

clip_predictions_lower=None, clip_predictions_upper=None,

conf_int=False, hcb_verbose=True, init_with_autoarima=False,

maxiter=50, method='lbfgs', name='sarimax', order=(1, 1, 2),

out_of_sample_size=0, scoring='mse', scoring_args=None,

seasonal_order=(1, 0, 2, 7), start_params=None,

suppress_warnings=False, trend=None, with_intercept=True)

[12]:

model

[12]:

SarimaxWrapper(always_search_model=False, autoarima_dict=None,

clip_predictions_lower=None, clip_predictions_upper=None,

conf_int=False, hcb_verbose=True, init_with_autoarima=False,

maxiter=50, method='lbfgs', name='sarimax', order=(1, 1, 2),

out_of_sample_size=0, scoring='mse', scoring_args=None,

seasonal_order=(1, 0, 2, 7), start_params=None,

suppress_warnings=False, trend=None, with_intercept=True)